![]()

LIBOR Market Model

Overview

The LIBOR Market Model (LMM) is an interest rate model

based on evolving LIBOR market forward rates.

It is also known as the Brace-Gatarek-Musiela (BGM) model, after the

authors of one of the first papers where it was introduced (Ref [2]). In contrast

to models that evolve the instantaneous short rate (Hull-White,

Black-Karasinski models) or instantaneous forward rates (Heath-Jarrow-Morton

model), which are not directly observable in the market, the objects modeled

using LMM are market-observable quantities (LIBOR forward rates). This makes LMM popular with market

practitioners. Another feature that

makes the LMM popular is that it is consistent with the market standard

approach for pricing caps using Black’s formula.

The LMM can be used to price any instrument whose pay-off

can be decomposed into a set of forward rates.

It assumes that the evolution of each forward rate is lognormal. Each forward rate has a time dependent volatility

and time dependent correlations with the other forward rates. After specifying these volatilities and

correlations, the forward rates can be evolved using

The standard lognormal LMM does not produce the

market-observed caplet volatility smile/skew (Ref [3]). To produce a

skew, the LMM can be extended to incorporate a local volatility model, a

stochastic volatility model, a jump diffusion model, or some combination of the

above. FINCAD provides pricing functions

that permit the use of three different versions of the LMM: (1) the standard

lognormal LMM, (2) the LMM enhanced with a Constant Elasticity of Variance

(CEV) local volatility process, and (3) the LMM enhanced with a Displaced

Diffusion (DD) local volatility process.

The next section discusses the standard lognormal LMM in detail. A sub-section at the end discusses the local

volatility extensions.

Formulas & Technical Details

Lognormal LIBOR Market Model

Assume that there are ![]() forward rates

forward rates ![]() that describe the

pay-off of an interest rate derivative.

The evolution of each forward rate

that describe the

pay-off of an interest rate derivative.

The evolution of each forward rate ![]() is described by

the stochastic differential equation:

is described by

the stochastic differential equation:

![]()

Equation 1

where

![]() is a standard Wiener

process and

is a standard Wiener

process and

![]() is the instantaneous

correlation between forward rates

is the instantaneous

correlation between forward rates ![]() and

and ![]() .

.

The instantaneous lognormal volatility and drift of

forward rate ![]() are

are ![]() and

and ![]() , respectively.

Note that the drift

, respectively.

Note that the drift ![]() for forward rate

for forward rate ![]() can be calculated

from the other forward rates and their instantaneous volatilities and

correlations (see Joshi for more details Ref [7]). Thus, the

instantaneous volatilities and correlations completely describe how forward

rates will evolve in the future. The

first thing to do is to specify the instantaneous volatilities and

correlations.

can be calculated

from the other forward rates and their instantaneous volatilities and

correlations (see Joshi for more details Ref [7]). Thus, the

instantaneous volatilities and correlations completely describe how forward

rates will evolve in the future. The

first thing to do is to specify the instantaneous volatilities and

correlations.

There are three main approaches for determining the

instantaneous volatilities and correlations of forward rates (Ref [12]):

1. They

can be obtained from analyzing historical data.

2. They

can be obtained by calibrating the model to current market prices of caplets

and European swaptions.

3. The

user can explicitly specify volatilities and correlations based on how he or

she believes they will evolve in the future.

A combination of these three approaches can also

be used.

Calibration

FINCAD provides functions for calibrating (see the Calibration FINCAD

Math Reference document) the instantaneous volatilities and correlations of the

LMM to quoted market data for caplets and European swaptions. The calibration of the LMM is a delicate

issue and is still an area of active research (Refs [3], [12], [13]). Calibrating

time-dependent instantaneous volatilities and correlations of a set of forward

rates to market data can be a difficult task.

To simplify the calibration procedure, the LMM calibration

functions use restricted functional forms (presented in recent literature Refs [3], [7], [6]) for the instantaneous volatilities and

correlations. The trade-off in using

restricted functional forms to make the calibration procedure easier is that

they may not be able to fit all market conditions. By calibrating using restricted functional

forms, the approach taken is really a combination of approaches 2 and 3 as

discussed in the previous section. This

is because choosing a functional form limits how forward rates can evolve in

the future. Even though calibration is

performed on market data, the choice of the functional form places restrictions

on how the rates can evolve.

The FINCAD LMM calibration functions use the following

functional form (or parameterization) for the instantaneous volatilities of

forward rates:

![]()

Equation 2

This linear-exponential parametric form is a

time-homogeneous form, which means that the instantaneous volatility of a forward

rate is not a function of the current date but only a function of the time

until the rate is set. The parameters ![]() allow for the

exact fitting of specific forward rate volatilities to quoted caplet volatilities.

This parametric form is able to produce both a monotonically decreasing and

“humped” structure of the instantaneous volatility, consistent with features

observed in the market. In addition, the parameters

allow for the

exact fitting of specific forward rate volatilities to quoted caplet volatilities.

This parametric form is able to produce both a monotonically decreasing and

“humped” structure of the instantaneous volatility, consistent with features

observed in the market. In addition, the parameters ![]() can be interpreted in

financial terms. For very long maturities i.e. when

can be interpreted in

financial terms. For very long maturities i.e. when ![]() is large, the

instantaneous volatility approaches

is large, the

instantaneous volatility approaches ![]() . Therefore we can interpret

. Therefore we can interpret ![]() as the

volatility of forward rates very far in the future. Generally, this parameter

should have a positive value. The parameter

as the

volatility of forward rates very far in the future. Generally, this parameter

should have a positive value. The parameter ![]() can be

interpreted as the rate at which the volatility approaches the limit

can be

interpreted as the rate at which the volatility approaches the limit ![]() . For forward rates with very short maturities, i.e.

when

. For forward rates with very short maturities, i.e.

when ![]() approaches zero, we

can see the instantaneous volatility approaches

approaches zero, we

can see the instantaneous volatility approaches ![]() . This leads us to conclude that this quantity should

also be greater than zero. We can gain some insight into the location of the

hump in the volatility structure by evaluating

. This leads us to conclude that this quantity should

also be greater than zero. We can gain some insight into the location of the

hump in the volatility structure by evaluating ![]() From this we find that the hump is located at

From this we find that the hump is located at ![]() Therefore, a hump will

only be present for

Therefore, a hump will

only be present for ![]() Under normal circumstances, we observe a volatility structure

similar to the one shown in the Figure 1 (using parameter values from Joshi [7] and Jaeckel [6]). The initial positive slope allows us to infer the

further restriction that

Under normal circumstances, we observe a volatility structure

similar to the one shown in the Figure 1 (using parameter values from Joshi [7] and Jaeckel [6]). The initial positive slope allows us to infer the

further restriction that ![]() in this case. For more

details see Brigo and Mercurio [3], Joshi [7] and Jaeckel [6].

in this case. For more

details see Brigo and Mercurio [3], Joshi [7] and Jaeckel [6].

Figure 1

The FINCAD LMM calibration functions use the

following functional form (or parameterization) for the instantaneous

correlations between forward rates:

![]()

Equation 3

This exponential parametric form is not time

dependent (i.e., it does not depend on the

current date nor the times until the two forward rates are set, but only on the

difference between the two times). It is

discussed by Molgedey [9]. It is also a

more general case of forms presented by Joshi [7] and Jaeckel [6]. The figure

below shows the instantaneous correlation for some parameter values used by

Joshi [7] and Jaeckel [6]. The general

interpretation of this structure is that forward rates with similar maturities

show a high degree of correlation, while those with very different maturities are

less correlated. We see that when ![]() , the correlation is 1 as required. The parameter

, the correlation is 1 as required. The parameter ![]() can be interpreted as

the limit of instantaneous correlation that is approached for rates far

separated in time, while the parameter

can be interpreted as

the limit of instantaneous correlation that is approached for rates far

separated in time, while the parameter ![]() describes how fast the

correlation decreases and approaches

describes how fast the

correlation decreases and approaches ![]() . In terms of an instantaneous correlation matrix, this

parametric form describes a matrix with ones along the diagonal and values

decreasing at a rate of

. In terms of an instantaneous correlation matrix, this

parametric form describes a matrix with ones along the diagonal and values

decreasing at a rate of ![]() as we move away from

the diagonal. The limit that the far off-diagonal elements approach is given by

as we move away from

the diagonal. The limit that the far off-diagonal elements approach is given by

![]() .

.

It should be noted that the above specification of the

instantaneous correlation between forward rates does not entirely describe the

“terminal correlation” between the rates. i.e. the non-instantaneous

correlation. The terminal correlation is determined by a combination of both

the instantaneous volatility and correlation structures. See Brigo and Mercurio

[3]

for more details.

Figure 2

The FINCAD LMM calibration functions allow:

·

a functional form for instantaneous volatilities

to be fitted to caplet data (caplet data contains no information about

correlations).

·

a functional form for instantaneous correlations

to be fitted to European swaption data given a specified form for instantaneous

volatilities (obtained from calibration to caplets).

·

functional forms for both instantaneous

volatilities and correlations to be fitted simultaneously to European swaption

data alone.

For example, the FINCAD calibration functions

allow a user to calibrate the instantaneous volatility and correlation

parameters by (1) calibrating the volatility parameters ![]() , and

, and ![]() to caplet data;

then (2) holding these parameters fixed while calibrating the instantaneous

correlation parameters

to caplet data;

then (2) holding these parameters fixed while calibrating the instantaneous

correlation parameters ![]() and

and ![]() to swaption data (see

the Calibration

FINCAD Math Reference document for more information).

to swaption data (see

the Calibration

FINCAD Math Reference document for more information).

The exact procedure by which caplets and swaptions are

used to calibrate the instantaneous volatilities and correlations depends on

the particular pricing application. For

example, one practitioner (Ref [6]) does not calibrate the instantaneous correlations at

all. Rather, the correlation parameters

are set to values based on historical data.

The volatility parameters ![]() ,

, ![]() are calibrated to

caplet data, then a forward rate-forward rate covariance matrix is constructed (see

Equation 4

below). This matrix is transformed into

a swap rate-swap rate covariance matrix, which is then calibrated to swaption

data. In this way one obtains a

“calibration to European swaption prices whilst retaining as much calibration

to the caplets as possible without violating the overall FRA/FRA correlation

structure too much, which is typically exactly what a practitioner wants for

the pricing of Bermuda swaptions” (Ref [6]). A similar

procedure using the FINCAD functions would be to (1) set the instantaneous

correlation parameters

are calibrated to

caplet data, then a forward rate-forward rate covariance matrix is constructed (see

Equation 4

below). This matrix is transformed into

a swap rate-swap rate covariance matrix, which is then calibrated to swaption

data. In this way one obtains a

“calibration to European swaption prices whilst retaining as much calibration

to the caplets as possible without violating the overall FRA/FRA correlation

structure too much, which is typically exactly what a practitioner wants for

the pricing of Bermuda swaptions” (Ref [6]). A similar

procedure using the FINCAD functions would be to (1) set the instantaneous

correlation parameters ![]() and

and ![]() to values suggested in

the literature (

to values suggested in

the literature (![]() , see Ref [6]); (2) use the FINCAD functions to calibrate the instantaneous

volatility parameters

, see Ref [6]); (2) use the FINCAD functions to calibrate the instantaneous

volatility parameters ![]() , and

, and ![]() ; to caplet data; then (3) use the FINCAD functions to calibrate

the instantaneous volatility and correlation parameters

; to caplet data; then (3) use the FINCAD functions to calibrate

the instantaneous volatility and correlation parameters ![]() ,

, ![]() , and

, and ![]() to swaption data, using

a narrow range of allowed values for each parameter centered on the values determined

in steps (1) and (2) (see the Calibration FINCAD Math Reference document for more information).

to swaption data, using

a narrow range of allowed values for each parameter centered on the values determined

in steps (1) and (2) (see the Calibration FINCAD Math Reference document for more information).

Calibrated values of the lognormal volatility and

correlation parameters typically lie in the ranges:

·

![]() : -1 to 1

: -1 to 1

·

![]() : 0 to 0.5

: 0 to 0.5

·

![]() : 0 to 5

: 0 to 5

·

![]() : 0 to 0.5

: 0 to 0.5

·

![]() : 0 to 1

: 0 to 1

·

![]() : 0 to 1

: 0 to 1

The performance of the calibration functions with

respect to determining volatility and correlation parameters depends on the

characteristics and quality of the caplet and swaption data. For example, calibration using illiquid or

inaccurate data (see Refs [3], [13]) may result in function failure or incorrect

parameter values. Also, because the

calibration functions use restricted parametric forms for instantaneous

volatilities and correlations, there will be cases when the functions fail even

when the market data is liquid and accurate.

In these cases, users will have to use a combination of the three

approaches (described at the end of the previous section) for determining

volatilities and correlations.

In order to make the calibration functions more efficient,

closed form approximations are used to price European swaptions that do not

require

Pricing

Evolving the Forward Rates using Monte Carlo

Simulation

After specifying which forward rates to evolve and their

instantaneous volatilities and correlations, by calibration or other means, a

In particular, an ![]() covariance matrix

covariance matrix ![]() is built for each

user-defined forward rate evolution period, where

is built for each

user-defined forward rate evolution period, where ![]() is the number of

forward rates. For example, given that

is the number of

forward rates. For example, given that ![]() is the forward

rate effective at

is the forward

rate effective at ![]() and terminating at

and terminating at

![]() , then for the time period

, then for the time period ![]() , where

, where ![]() , the elements of the

, the elements of the ![]() instantaneous

covariance matrix are:

instantaneous

covariance matrix are:

![]() .

.

Equation

4

The

covariance matrix ![]() contains all the

information needed to evolve the forward rates from time

contains all the

information needed to evolve the forward rates from time ![]() to

to ![]() and can be

calculated from the restricted functional forms for instantaneous volatilities

and correlations. In particular, the

parameterization of instantaneous correlation in Equation 3 is time-independent, which means that instantaneous

correlation can be taken out of the covariance integral in Equation 4. The resulting integral can

be evaluated analytically using the functional form for instantaneous

volatility from Equation

2 (see Jaeckel [6]).

and can be

calculated from the restricted functional forms for instantaneous volatilities

and correlations. In particular, the

parameterization of instantaneous correlation in Equation 3 is time-independent, which means that instantaneous

correlation can be taken out of the covariance integral in Equation 4. The resulting integral can

be evaluated analytically using the functional form for instantaneous

volatility from Equation

2 (see Jaeckel [6]).

If the pay-off of the

instrument depends on the value of the forward rates ![]() at one future time

at one future time

![]() , the forward rates only have to be evolved for a single

time step from the value date

, the forward rates only have to be evolved for a single

time step from the value date ![]() to

to ![]() . This requires

only a single

. This requires

only a single ![]() covariance matrix

for time period t0 to t1 to describe the evolution of forward rates. If the payoff of the instrument depends on

the forward rates observed at

covariance matrix

for time period t0 to t1 to describe the evolution of forward rates. If the payoff of the instrument depends on

the forward rates observed at ![]() dates

dates ![]() ,

, ![]() , …

, … ![]() , the forward rates need to be evolved for m time steps from

, the forward rates need to be evolved for m time steps from ![]() 0 to

0 to ![]() ,

, ![]() to

to ![]() , …

, … ![]() to

to ![]() . To specify the

evolution of forward rates requires

. To specify the

evolution of forward rates requires ![]() separate

covariance matrices, one for each time evolution period.

separate

covariance matrices, one for each time evolution period.

Given the matrix

elements ![]() for a particular

time evolution period,

for a particular

time evolution period, ![]() is decomposed into

a pseudo square root via the Cholesky method, or via spectral decomposition if

the Cholesky method fails for any reason:

is decomposed into

a pseudo square root via the Cholesky method, or via spectral decomposition if

the Cholesky method fails for any reason:

![]() .

.

Equation 5

Equation

1 is then written as (Ref [6]):

![]()

Equation 6

where the ![]() are

are ![]() independent Wiener

processes. If one wishes to employ

“factor reduction” and evolve the forward rates using

independent Wiener

processes. If one wishes to employ

“factor reduction” and evolve the forward rates using ![]() independent Wiener

processes (Ref [6]), then Equation

1 is re-written as:

independent Wiener

processes (Ref [6]), then Equation

1 is re-written as:

![]() .

.

Equation 7

The

variances of the forward rates, ![]() , (obtained from calibration or directly from the

market-quoted implied volatilities of caplets) are retained by setting (Ref [6]):

, (obtained from calibration or directly from the

market-quoted implied volatilities of caplets) are retained by setting (Ref [6]):

.

.

Equation 8

The FINCAD

implementation of the LMM uses the zero coupon bond maturing at time ![]() (i.e., on the terminating date of the

(i.e., on the terminating date of the ![]() forward rate,

forward rate, ![]() ) as numeraire, so the drift of

) as numeraire, so the drift of ![]() at time

at time ![]() is given by (Refs [3], [6]):

is given by (Refs [3], [6]):

.

.

Equation

9

![]() is the accrual

factor for the rate term defined by

is the accrual

factor for the rate term defined by ![]() .

.

Because the drifts given

by Equation

9 are state dependent and therefore indirectly

stochastic, Equation

1 must be solved using a numerical scheme. FINCAD implements a log-Euler discretization

of the forward rate process (Refs [3], [6]):

![]() .

.

Equation

10

![]() is the drift from Equation 9, predicted using Equation 4 for the period

is the drift from Equation 9, predicted using Equation 4 for the period ![]() , then corrected using the “predictor-corrector” method (Ref

[6]) to take into account the fact that the

, then corrected using the “predictor-corrector” method (Ref

[6]) to take into account the fact that the ![]() change during the

evolution period.

change during the

evolution period.

Forward rates in the

standard lognormal LMM are evolved over successive time periods in a Monte

Carlo simulation according to Equation

10, given the forward rate-forward rate covariance matrix

![]() for each time

period. By generating many such paths of

forward rates, the expectation of a particular forward rate on a particular

date in the chosen probability measure (i.e., the

for each time

period. By generating many such paths of

forward rates, the expectation of a particular forward rate on a particular

date in the chosen probability measure (i.e., the ![]() -forward measure or terminal measure), conditional on

today’s value of the forward rate, is the average simulated value over all

paths. On each path of forward rates,

the coupons and the price of the numeraire asset are calculated on coupon

payment dates. Today’s value of the

numeraire asset is also calculated for the path. The coupons are discounted through the

numeraire and summed to get the price of the instrument on the path. The fair value of the instrument is found by

averaging over all paths.

-forward measure or terminal measure), conditional on

today’s value of the forward rate, is the average simulated value over all

paths. On each path of forward rates,

the coupons and the price of the numeraire asset are calculated on coupon

payment dates. Today’s value of the

numeraire asset is also calculated for the path. The coupons are discounted through the

numeraire and summed to get the price of the instrument on the path. The fair value of the instrument is found by

averaging over all paths.

User Defined Covariance Matrices

An input to the FINCAD

interest rate derivative pricing functions that use the LMM is a sequence of

covariance matrices, one for each time evolution period of the instrument. Utility functions are provided to generate

these covariance matrices, given the parametric forms for instantaneous

volatilities and correlations described above.

Instead of using the

calibration and matrix generation functions, users can define their own

covariance matrices and input them directly into the pricing functions. The following example describes how this can

be done.

The example assumes

an instrument whose pay-off depends on 4 forward rates. The first forward rate ![]() is from

is from ![]() , the second forward rate

, the second forward rate ![]() is from

is from ![]() , the third forward rate

, the third forward rate ![]() is from

is from ![]() , the fourth forward

rate

, the fourth forward

rate ![]() is from

is from ![]() and the current

date corresponds to time

and the current

date corresponds to time ![]() . Also, suppose

this instrument has a Bermudan structure and its pay-off depends on the forward

rates observed at times

. Also, suppose

this instrument has a Bermudan structure and its pay-off depends on the forward

rates observed at times ![]() , and

, and ![]() . Running the

simulation requires evolving the forward rates from

. Running the

simulation requires evolving the forward rates from ![]() ,

, ![]() ,

, ![]() and

and ![]() . Thus, four

separate 4 by 4 covariance matrices are required to describe the evolution of

forward rates, one for each time step that needs to be evolved.

. Thus, four

separate 4 by 4 covariance matrices are required to describe the evolution of

forward rates, one for each time step that needs to be evolved.

Now, suppose the user

wants to explicitly specify the instantaneous volatilities and correlations as

piece-wise constant functions (i.e.,![]() and

and ![]() are constants during

each time step) with the following values:

are constants during

each time step) with the following values:

From t0

to t1,

From t1

to t2,

From t2

to t3,

From t3

to t4,

Notice that the data

has a certain structure. For each time

period ![]() and

and ![]() if

if ![]() . This is because

for

. This is because

for ![]() i forward

rate

i forward

rate ![]() has already

expired because it is already past its starting time

has already

expired because it is already past its starting time ![]() . Forward rates

that have already expired cannot be evolved so they do not have volatilities

and correlations. So for this example,

from

. Forward rates

that have already expired cannot be evolved so they do not have volatilities

and correlations. So for this example,

from ![]() , the forward rates

, the forward rates ![]() have to be evolved;

from

have to be evolved;

from ![]() , forward rates

, forward rates ![]() have to be evolved;

from

have to be evolved;

from ![]() , forward rates

, forward rates ![]() have to be evolved; and from

have to be evolved; and from ![]() , only

, only ![]() has to be evolved.

has to be evolved.

Also, notice that the

non-zero diagonals of the instantaneous correlation matrix are always one and

the matrix is symmetric. This is because the correlation between ![]() and

and ![]() is the same as

that between

is the same as

that between ![]() and

and ![]() . Another

restriction on the instantaneous correlation matrix is that is it positive

definite. For more on restrictions for

instantaneous volatilities and correlations, see Ref [3].

. Another

restriction on the instantaneous correlation matrix is that is it positive

definite. For more on restrictions for

instantaneous volatilities and correlations, see Ref [3].

Given values for the

instantaneous volatilities and correlations, Equation 4 is then used to generate the covariance matrices. Because the instantaneous volatilities and

correlations are piecewise-constant, the integral is easy to evaluate. For example, to calculate the entry ![]() suppose that

suppose that ![]() and

and ![]() (in years). From Equation 4,

(in years). From Equation 4, ![]() using the values of

using the values of ![]() between

between ![]() and

and ![]() . Thus,

. Thus, ![]() .

.

Early Exercise in Monte

Carlo Simulation

When there is only

one possible exercise date (European exercise),

The FINCAD LMM

implementation uses the Least Squares Monte Carlo (LSMC) algorithm proposed by

Longstaff and Schwartz [8] to price instruments with early exercise

features. The LSMC algorithm works

backwards from the last exercise date to previous exercise dates as follows:

1. Calculate

the exercise value on the exercise date for each path. For Bermudan swaptions, the exercise value is

simply the value of the underlying swap, which is easily calculated “off the

curve” (Ref [12]).

2.

If this is the last exercise date, set the

continuation value = discounted continuation value = 0 for each path and go to

Step 6.

3.

For each path, set the continuation value on the

exercise date equal to the discounted continuation value from the later

exercise date.

4.

Regress the continuation values from each path

in Step 3 against a linear combination of “basis functions” evaluated at

“regression variables”.

5.

Use the regression parameters, regression

variables, and basis functions from Step 4 to estimate the continuation value

on the exercise date for each path.

6.

For each path, if the exercise value >

continuation value, then set the exercise flag for this date = TRUE and set

continuation value = exercise value. Otherwise,

set the exercise flag = FALSE and set continuation value = discounted

continuation value.

7.

Move to the previous exercise date.

8.

Repeat steps 1-7 until there are no more

exercise dates.

The earliest

date on each path for which exercise flag = TRUE is the optimal exercise date

for that path.

The exercise

strategy found by the LSMC algorithm is typically a sub-optimal exercise

strategy (at best, the optimal exercise strategy), so the price of the option

given by the LSMC algorithm is a lower bound on the price.

The choice of

regression variables and choice of basis functions affect how closely the LSMC

algorithm approximates the optimal exercise strategy, and depend on the

specific instrument being priced (Refs [8], [12]). The FINCAD

pricing functions provide a choice between two sets of regression

variables: either the 0th and

1st moments of the interest rate curve (i.e.,

the level and slope of the interest rate curve, represented by a swap price per

unit notional and a forward rate) or the sums of the random factors used to

evolve each forward rate. A choice

between two different sets of basis functions is also provided: either 2nd-order polynomials or 2nd-order

Laguerre polynomials. The price of an

instrument, e.g., a Bermudan swaption, is not

expected to be particularly sensitive to the basis functions. Instead, one should focus on selecting

regression variables that are indicative of continuation values relative to

exercise values (Ref [12]). The sums of

random factors are general variables that can be used for any derivative. In the case of swaptions, the 0th

and 1st moments of the interest rate curve are expected to be the

best choice for regression variables.

For more details on the choice of regression variables and basis

functions for Bermudan swaptions see Pedersen [11] and Piterbarg [12].

The LSMC algorithm is

described further in the Bermudan and American Style

Basket Options FINCAD Math Reference document.

Local Volatility Extensions

FINCAD provides two

local volatility extensions to the LMM in order to model implied volatility

skew: Constant Elasticity of Variance

(CEV) and Displaced Diffusion (DD).

Constant Elasticity of Variance

In the LMM

with CEV, Equation

1 becomes (Refs [5], [10], [14]):

![]()

Equation

11

so that Equation 9 becomes (Refs [1], [5], [10]):

.

.

Equation 12

and Equation 10 becomes (Refs [1], [5], [10]):

Equation

13

where ![]() is the CEV parameter,

constant for all forward rates. That is,

forward rates in the LMM+CEV are evolved over successive time periods in a

Monte Carlo simulation according to Equation 13, given

is the CEV parameter,

constant for all forward rates. That is,

forward rates in the LMM+CEV are evolved over successive time periods in a

Monte Carlo simulation according to Equation 13, given ![]() and the forward

rate-forward rate CEV covariance matrix for each time period. The parameterization of CEV instantaneous

volatility and correlation for calibration of the covariance matrix retain the

same forms as shown in Equation

2 and Equation

3, respectively.

The standard LMM is recovered from the LMM+CEV by simply setting

and the forward

rate-forward rate CEV covariance matrix for each time period. The parameterization of CEV instantaneous

volatility and correlation for calibration of the covariance matrix retain the

same forms as shown in Equation

2 and Equation

3, respectively.

The standard LMM is recovered from the LMM+CEV by simply setting ![]() .

.

Note that Equation 13 is the log-Euler discretization of Equation 11. In a process

such as CEV where forward rate = 0 is possible, it is typically better to use a

direct Euler discretization of the stochastic differential equation (Ref [1]). However, for

typical market conditions where forward rate = 0 is improbable, the log-Euler

discretization works well.

Closed-form

expressions for the prices of caplets and European swaptions are available (Refs

[1], [3], [5], [10]) for calibration of the LMM+CEV. Typical values of the calibrated model

parameters are ![]() ,

, ![]() ,

, ![]() , and

, and ![]() for a negative

skew (caplet implied volatility decreases with strike rate), or

for a negative

skew (caplet implied volatility decreases with strike rate), or ![]() ,

, ![]() ,

, ![]() , and

, and ![]() for a positive skew

(caplet implied volatility increases with strike rate). When calibrating the LMM+CEV, one must

usually input large uncertainties for the calibration instruments (caplets or

swaptions) that are far from the money (see the Calibration

FINCAD Math Reference document), because these instruments have near-zero vega

which means the same price is obtained for a large range of volatilities.

for a positive skew

(caplet implied volatility increases with strike rate). When calibrating the LMM+CEV, one must

usually input large uncertainties for the calibration instruments (caplets or

swaptions) that are far from the money (see the Calibration

FINCAD Math Reference document), because these instruments have near-zero vega

which means the same price is obtained for a large range of volatilities.

Displaced Diffusion

In the LMM with

DD, Equation

1 becomes (Refs [7], [10], [14]):

![]()

Equation

14

so that Equation 9 becomes (Refs [1], [7], [10]):

.

.

Equation 15

and Equation 10 becomes (Refs [1], [3], [10], [14]):

![]()

Equation

16

where ![]() is the DD

parameter, constant for all forward rates.

That is, forward rates in the LMM+DD are evolved over successive time

periods in a Monte Carlo simulation according to Equation 16, given

is the DD

parameter, constant for all forward rates.

That is, forward rates in the LMM+DD are evolved over successive time

periods in a Monte Carlo simulation according to Equation 16, given ![]() and the forward

rate-forward rate DD covariance matrix for each time period. The parameterization of DD instantaneous

volatility and correlation for calibration of the covariance matrix retain the

same forms as shown in Equation

2 and Equation

3, respectively.

The standard LMM is recovered from the LMM+DD by simply setting

and the forward

rate-forward rate DD covariance matrix for each time period. The parameterization of DD instantaneous

volatility and correlation for calibration of the covariance matrix retain the

same forms as shown in Equation

2 and Equation

3, respectively.

The standard LMM is recovered from the LMM+DD by simply setting ![]() = 0.

= 0.

Closed-form

expressions for the prices of caplets and European swaptions are available (Refs

[3], [10]) for calibration of the LMM+DD. Typical values of the calibrated model

parameters are ![]() ,

, ![]() ,

, ![]() , and

, and ![]() for a negative

skew (caplet implied volatility decreases with strike rate), or

for a negative

skew (caplet implied volatility decreases with strike rate), or ![]() ,

, ![]() ,

, ![]() , and

, and ![]() for a positive

skew (caplet implied volatility increases with strike rate). When calibrating the LMM+DD, one must usually

input large uncertainties for the calibration instruments (caplets or

swaptions) that are far from the money (see the Calibration

FINCAD Math Reference document), because these instruments have near-zero vega

which means the same price is obtained for a large range of volatilities.

for a positive

skew (caplet implied volatility increases with strike rate). When calibrating the LMM+DD, one must usually

input large uncertainties for the calibration instruments (caplets or

swaptions) that are far from the money (see the Calibration

FINCAD Math Reference document), because these instruments have near-zero vega

which means the same price is obtained for a large range of volatilities.

FINCAD Functions

aaCovarMatGen2_LMM (d_v, period_date_tbl,

fwdrate_tbl, acc, model_vol, model_cor, model_parms, scalfac_tbl)

Generates a sequence of forward rate - forward rate

covariance matrices using the LIBOR Market Model. The covariance matrices are used to evolve

forward rates over sequential time periods.

Functional forms are used for instantaneous volatilities and

correlations.

aaSwaption_eu_LMM

(d_v, fwdrate_tbl, npa, cpn, acc, swpn, df_crv, intrp, approx, covar_mat, stat)

Calculates the fair value for a European style swaption

using the LIBOR Market Model with closed form analytic approximations.

aaSwaption2_eu_LMM_ff

(d_v, d_e, d_m, princ, cpn, freq, acc, d_rul, swpn, hl, approx, model_vol,

model_cor, model_parms, scalfac_tbl, df_crv, intrp, stat)

Calculates fair value for a European style swaption using

the LIBOR Market Model with local volatility.

Closed-form analytic approximations are used for valuation, and

functional forms are used for instantaneous volatilities and correlations.

aaCaplet_LMM(r_option_type,

princ, d_v, d_exp, d_e, d_t, rate_ex, acc, model_vol, model_parms, scalfac_tbl,

df_crv, intrp, stat)

Calculates fair value of a caplet or floorlet using the LIBOR

Market Model with local volatility.

aaCapletVltGen_LMM(d_v,

d_e, acc, vol_tbl, scale_fact)

Generates the Black volatility of a caplet or floorlet

using a functional form for the instantaneous volatility in the LIBOR Market

Model.

aaSwaption_LMM_fs(d_v, swap_tbl,

acc_pay, acc_rate, swpn, df_crv, intrp, covar_mat, num_fact, reg_var, basis_fn,

num_rnd, table_type)

Calculates the fair

value of a Bermudan style swaption with the LIBOR Market Model using

aaSwaption_LMM_LV_fs(d_v, swap_tbl,

acc_pay, acc_rate, swpn, df_crv, intrp, covar_mat, num_fact, lv_model,

lv_param, reg_var, basis_fn, num_rnd, table_type)

Calculates the fair

value of a Bermudan style swaption with the LIBOR Market Model and local

volatility using

aaSwaption_LMM_fs_tbl(d_v, swap_tbl,

table_type)

Generates a table of

rate evolution periods or rate terms for a swaption.

Description of Inputs

|

Input Argument |

Type |

Description |

|

d_v |

Date |

Valuation (Settlement) Date. |

|

d_e |

Date |

Effective Date. |

|

d_m |

Date |

Maturity Date. |

|

d_t |

Date |

Terminating Date. |

|

d_exp |

Date |

Expiry Date. |

|

npa, princ |

Number |

Notional Principal Amount. |

|

cpn |

Number |

Coupon Rate. |

|

freq |

Number |

Frequency. |

|

acc, acc_pay, acc_rate |

Number |

Day Count Convention. |

|

r_option_type, swpn |

Number |

Option Type. |

|

rate_ex |

Rate |

Exercise Rate. |

|

d_rul |

Number |

Business Day Convention. |

|

swpn |

Number |

Specify as either a payer or receiver swaption. |

|

hl |

Table |

|

|

df_crv |

Table |

Discount Factor Curve. |

|

intrp |

Number |

Interpolation Method. |

|

model_vol |

Number |

Parameterization of instantaneous volatility. |

|

model_cor |

Number |

Parameterization of instantaneous correlation. |

|

model_parms |

Table |

Table containing values of instantaneous volatility and

correlation parameters. |

|

scalfac_tbl |

Table |

Volatility scale factor table for forward rates. This table can be entered as a 3-column

table (effective date, terminating date, scale factor) or as a single cell containing

a single scale factor that is applied to the model-predicted volatilities of

all forward rates. |

|

scale_fact |

|

Volatility scale factor for a single forward rate. |

|

vol_tbl |

Table |

Table specifying the parameters for a functional form of

instantaneous volatility. |

|

swap_tbl |

|

Swap coupon table.

This is an N×9 table, where the columns are rate effective date, rate

terminating date, coupon effective date, coupon terminating date, notional

principal amount, coupon, margin above or below a floating rate, exercise

flag, and exercise fee (% of notional).

The dates must be input already adjusted for holidays, weekends, and a

business day convention. All rates are

input as annualized rates. Each row of the swap table corresponds to a coupon period.

The columns of the table are specified as follows: 1.

Both rate terms and coupon periods must be

contiguous. That is, the terminating date in one row of the table must be the

effective date in the next row of the table. 2. There

is one rate per coupon period. The

rate effective date must be on or before the coupon terminating date. The rate can set in advance or in arrears

by adjusting the rate effective and terminating dates relative to the coupon

effective and terminating dates.

In-arrears pricing is handled via 3. A

forward rate is evolved in 4. The

coupon periods apply to both the fixed and floating legs of the swap. 5. The

coupon is the annualized rate on the fixed leg; the margin is the annualized

margin on the floating leg. An exercise flag > 0 means that the option to enter the

underlying swap is exercisable on the coupon effective date. |

|

lv_model |

Number |

Local volatility model. |

|

lv_param |

Number |

Local volatility parameter. |

|

period_date_tbl |

Table |

Table containing starting and end dates for a set of time

periods to generate covariance matrices for the forward rates. |

|

fwdrate_tbl |

Table |

Table containing effective and terminating dates for a set

of forward rates. |

|

covar_mat |

Table |

Table containing a covariance matrix (or sequence of

covariance matrices) describing the evolution of a set of forward rates. |

|

approx |

Number |

Approximate closed-form expression for valuing a European

swaption in the Libor Market Model. |

|

num_fact |

Number |

Maximum number of factors to use in |

|

reg_var |

Number |

Choice of regression variables in LSMC algorithm. |

|

basis_fn |

|

Choice of basis functions in LSMC algorithm. |

|

num_rnd |

Table |

Number of |

|

stat |

Number |

Statistic to be output. |

|

table_type |

Number |

Type of table to output. |

Description of Outputs

aaCovarMatGen2_LMM

|

Output |

Type |

Description |

|

covar_mat |

Table |

Table containing a sequence of covariance matrices |

aaSwaption_eu_LMM, aaSwaption2_eu_LMM_ff

|

Output Statistics |

Type |

Description |

|

1 |

Number |

option price |

|

2 |

Rate |

swaption Black volatility |

|

3 |

Rate |

par swap rate |

aaCaplet_LMM

|

Output Statistics |

Type |

Description |

|

1 |

Number |

caplet/floorlet price |

|

2 |

Rate |

caplet/floorlet Black volatility |

|

3 |

Rate |

implied forward rate |

aaCapletVltGen_LMM

|

Output |

Type |

Description |

|

caplet_vol |

Number |

caplet Black volatility |

aaSwaption_LMM_fs, aaSwaption_LMM_LV_fs

table_type = 1, ROW 1 = average over all paths, ROW 2 =

accuracy

|

Column |

Type |

Description |

|

1 |

Number |

Option price |

|

2 |

Number |

Expected time of exercise (in years) |

|

3 |

Number |

Probability of exercise |

aaSwaption_LMM_fs_tbl

table_type = 1

|

Column |

Type |

Description |

|

1 |

Date |

Effective date of evolution period |

|

2 |

Date |

Terminating date of evolution period |

table_type = 2

|

Column |

Type |

Description |

|

1 |

Date |

Effective date of rate term |

|

2 |

Date |

Terminating date of rate term |

Example

Valuation of Bermudan Swaptions

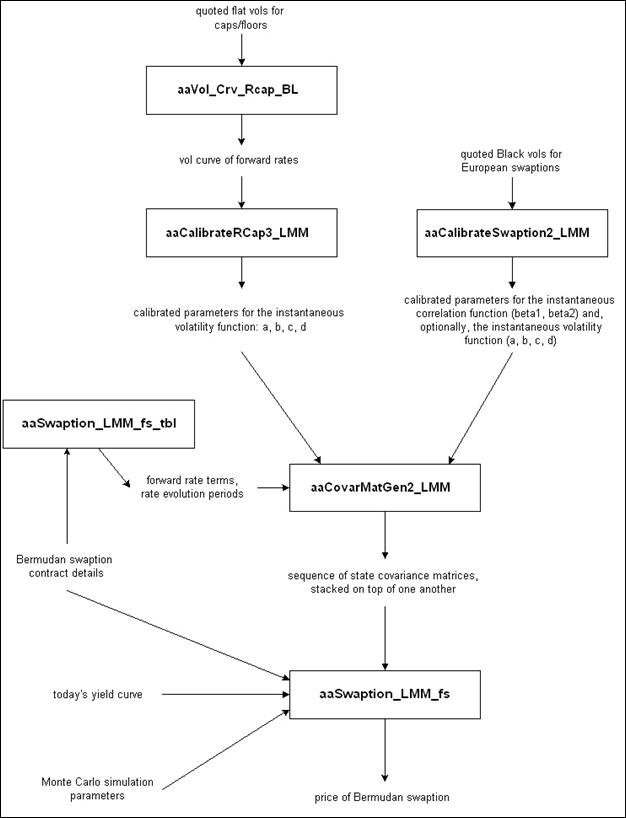

This example shows how to value a Bermudan swaption in the

LMM using aaSwaption_LMM_fs. The flow of data through the FINCAD functions

is shown in Figure

3.

Note that the flow of data for aaSwaption_LMM_LV_fs,

which uses the LMM enhanced with local volatility, is identical to that shown

in Figure

3 except that (1) aaSwaption_LMM_fs

is replaced by aaSwaption_LMM_LV_fs;

(2) aaCalibrateRCap3

and aaCalibrateSwaption2_LMM

output an additional parameter, namely, the local volatility parameter, gamma;

(3) gamma is input directly into aaSwaption_LMM_LV_fs. The other model parameters (a, b, c, d,

beta1, beta2) are still input into aaCovarMatGen2_LMM in order to produce the

sequence of covariance matrices.

Figure 3:

Data flow through FINCAD functions in order to price a Bermudan swaption

using the LIBOR Market Model.

Assume the Bermudan swaption being valued has settlement

date of 14-Feb-2000, an effective date of 15-Mar-2000 and a maturity date of 15-Mar-2004. An accrual method of 30/360, no business day

adjustments and linear interpolation are used for all calculations. The fixed and floating payments are both

annual, the principal amount is 100, the fixed coupon is 5.0% and the swaption

is the right to receive fixed.

First we generate the rate terms and coupon periods using aaDateGen

with the following inputs:

aaDateGen

|

Argument |

Description |

Example Data |

Switch |

|

d_s |

settlement date |

14-Feb-2000 |

|

|

d_t |

terminating date |

15-Mar-2004 |

|

|

d_e |

effective date |

15-Mar-2000 |

|

|

d_f_cpn |

date of first coupon after effective date |

omitted |

|

|

d_l_cpn |

date of last coupon prior to terminating date |

omitted |

|

|

freq |

cash flow frequency |

1 |

annual |

|

hl |

holiday list |

empty (for simplicity) |

|

|

d_rul |

business day convention |

1 |

no date adjustment |

|

table_type |

table type |

2 |

two-column array |

The output rate terms and coupon periods are:

Output Table 1 – rate terms/coupon periods

|

Effective Date |

Terminating Date |

|

15-Mar-2000 |

15-Mar-2001 |

|

15-Mar-2001 |

15-Mar-2002 |

|

15-Mar-2002 |

15-Mar-2003 |

|

15-Mar-2003 |

15-Mar-2004 |

Given the coupon periods and rate terms, we build

the swap table:

t_1225 – swap table

|

rate eff date |

rate term date |

coupon eff date |

coupon term date |

NPA |

cpn |

margin |

ex flag |

ex fee |

|

15-Mar-2000 |

15-Mar-2001 |

15-Mar-2000 |

15-Mar-2001 |

100 |

5.0% |

0.0% |

1 |

0.0% |

|

15-Mar-2001 |

15-Mar-2002 |

15-Mar-2001 |

15-Mar-2002 |

100 |

5.0% |

0.0% |

1 |

0.0% |

|

15-Mar-2002 |

15-Mar-2003 |

15-Mar-2002 |

15-Mar-2003 |

100 |

5.0% |

0.0% |

1 |

0.0% |

|

15-Mar-2003 |

15-Mar-2004 |

15-Mar-2003 |

15-Mar-2004 |

100 |

5.0% |

0.0% |

1 |

0.0% |

We now generate the evolution periods

and forward rates for

aaSwaption_LMM_fs_tbl

|

Argument |

Description |

Example Data |

Switch |

|

d_v |

value date |

14-Feb-2000 |

|

|

swap_tbl |

swap table |

t_1225 (above) |

|

|

table_type |

table type |

1…2 |

period dates table or forward rate table |

The evolution periods (table_type = 1) and forward

rates (table_type = 2) from aaSwaption_LMM_fs_tbl are:

Output Table 2 – period dates table

|

Effective Date |

Terminating Date |

|

14-Feb-2000 |

15-Mar-2000 |

|

15-Mar-2000 |

15-Mar-2001 |

|

15-Mar-2001 |

15-Mar-2002 |

|

15-Mar-2002 |

15-Mar-2003 |

Output Table 3 –forward rate table

|

Effective Date |

Terminating Date |

|

15-Mar-2000 |

15-Mar-2001 |

|

15-Mar-2001 |

15-Mar-2002 |

|

15-Mar-2002 |

15-Mar-2003 |

|

15-Mar-2003 |

15-Mar-2004 |

Note that the list of forward rates in Output

Table 3 includes all rates from the swap table above (t_1225), because all of

these rates set in the future (i.e., after

the Value Date). Also note that there

are 4 rate evolution periods in Output Table 2.

To price the swaption, forward rates need to be evolved to each of the

rate effective dates. Rates also need to

be evolved to all coupon terminating dates (except the last one) because the swaption

is exercisable on these dates. These swaption

exercise dates coincide with the rate effective dates, so we need only consider

the rate effective dates when determining the rate evolution periods, which is

why there are 4 periods in Output Table 2.

The function aaCovarMatGen2_LMM

can be used to generate the sequence of covariance matrices required as an

input to aaSwaption_LMM_fs. Suppose that aaCalibrateSwaption2_LMM

has been used to calibrate the LMM to swaptions, with the 4-parameter linear-exponential

parametric form for instantaneous lognormal volatilities, the exponential form

for instantaneous correlations, and volatility scale factors set to 1 (see the Calibration

FINCAD Math Reference document).

Alternatively we could have used aCalibrateRCap3_LMM

to calibrate the instantaneous lognormal volatility parameters (![]() ), then used aaCalibrateSwaption2_LMM to calibrate the

instantaneous correlation parameters (

), then used aaCalibrateSwaption2_LMM to calibrate the

instantaneous correlation parameters (![]() and

and ![]() ). The calibrated

parameter values are assembled in Output Table 4.

). The calibrated

parameter values are assembled in Output Table 4.

Output Table 4 – Model Parameters

|

a |

b |

c |

d |

beta1 |

beta2 |

|

-0.02 |

0.3 |

2 |

0.16 |

0.1 |

0.1 |

Output Tables 2 through 4 are used by aaCovarMatGen2_LMM

to generate the covariance matrices for the Bermudan swaption. The complete list of inputs to aaCovarMatGen2_LMM

is shown below.

aaCovarMatGen2_LMM

|

Argument |

Description |

Example Data |

Switch |

|

d_v |

Valuation (settlement) date |

14-Feb-2000 |

|

|

period_date_tbl |

Table containing starting and end dates for a set of time

periods |

Output Table 2 (above) |

|

|

fwdrate_tbl |

Table containing effective and terminating dates for a set

of forward rates |

Output Table 3 (above) |

|

|

acc |

Day count convention |

4 |

30/360 |

|

model_vol |

Parameterization of instantaneous volatility |

1 |

4-parameter linear exponential |

|

model_cor |

Parameterization of instantaneous correlation |

1 |

2-parameter exponential |

|

model_parms |

Table containing values of all model parameters |

Output Table 4 (above) |

|

|

scalfac_tbl |

Volatility scale factor table for forward rates. |

1 |

|

Output Table 5 shows the sequence of four 4x4 covariance

matrices generated by aaCovarMatGen2_LMM, which is used to evolve

the 4 forward rates over the 4 time periods.

Output Table 5 – Covariance Matrix Sequence

|

0.00202425 |

0.00236746 |

0.00187570 |

0.00163840 |

|

0.00236746 |

0.00332062 |

0.00262800 |

0.00229292 |

|

0.00187570 |

0.00262800 |

0.00248774 |

0.00216844 |

|

0.00163840 |

0.00229292 |

0.00216844 |

0.00226080 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.03864862 |

0.03258181 |

0.02709047 |

|

0.00000000 |

0.03258181 |

0.03333816 |

0.02760589 |

|

0.00000000 |

0.02709047 |

0.02760589 |

0.02736581 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.00000000 |

0.03864862 |

0.03258181 |

|

0.00000000 |

0.00000000 |

0.03258181 |

0.03333816 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.00000000 |

|

0.00000000 |

0.00000000 |

0.00000000 |

0.03864862 |

Finally we call aaSwaption_LMM_fs. We select 2nd order polynomials as

basis functions and the 1st two moments of the interest rate curve

as regression variables (as described under Formulas

& Technical Details above).

We use all possible random factors, which in this case is 4 (the maximum

number of stochastic rates in any one period is 4) and we use 1000

t_43_32 – discount factor curve

|

grid date |

discount factor |

|

14-Feb-2000 |

1.00000000 |

|

15-Feb-2000 |

0.99986634 |

|

15-Aug-2000 |

0.97583485 |

|

15-Feb-2001 |

0.95212637 |

|

15-Aug-2001 |

0.92936652 |

|

15-Feb-2002 |

0.90678702 |

|

15-Aug-2002 |

0.88511098 |

|

15-Feb-2003 |

0.86360669 |

|

15-Aug-2003 |

0.84296283 |

|

15-Feb-2004 |

0.82248256 |

|

15-Aug-2004 |

0.80271444 |

|

15-Feb-2005 |

0.78321202 |

|

15-Aug-2005 |

0.76448994 |

|

15-Feb-2006 |

0.74591621 |

|

15-Aug-2006 |

0.72808566 |

|

15-Feb-2007 |

0.71039639 |

|

15-Aug-2007 |

0.69341491 |

|

15-Feb-2008 |

0.67656799 |

|

15-Aug-2008 |

0.66030689 |

|

15-Feb-2009 |

0.64426435 |

|

15-Aug-2009 |

0.62886370 |

|

15-Feb-2010 |

0.61358509 |

|

15-Aug-2010 |

0.59891781 |

|

14-Feb-2011 |

0.58439810 |

|

14-Feb-2012 |

0.55648080 |

|

14-Feb-2013 |

0.52982607 |

|

14-Feb-2014 |

0.50451573 |

|

14-Feb-2015 |

0.48041449 |

aaSwaption_LMM_fs

|

Argument |

Description |

Example Data |

Switch |

|

d_v |

value (settlement) date |

14-Feb-2000 |

|

|

swap_tbl |

swap table |

t_1225 (above) |

|

|

acc_pay |

accrual method for coupon periods |

4 |

30/360 |

|

acc_rate |

accrual method for rate terms |

4 |

30/360 |

|

df_crv |

discount factor curve |

t_43_32 (above) |

|

|

intrp |

interpolation method |

1 |

linear |

|

covar_mat |

covariance matrix |

Output Table 5 (above) |

|

|

num_fact |

maximum number of stochastic factors per period |

4 |

|

|

reg_var |

regression variables |

1 |

IR curve moments |

|

basis_fn |

basis functions |

1 |

polynomial |

|

num_rnd |

number of random trials |

1000.5 |

|

|

table_type |

table type |

1 |

price table |

The output price table, showing price (1st

row) and accuracy (2nd row) is:

Output Table 6 – price table

|

Option price |

Expected time of exercise (in years) |

Probability of exercise |

|

1.181049 |

2.447973 |

0.575075 |

|

0.113669 |

0.128543 |

0.037544 |

The 95% confidence interval for the option price is:

[1.181049 – 0.113669, 1.181049 + 0. 113669] = [1.067381, 1.294718].

Accuracy values can be made smaller by increasing

the number of

Related Functions

aaCalibrateRcap2_LMM,

aaCalibrateRcap3_LMM,

aaCalibrateSwaption2_LMM,

aaVol_Crv_Rcap_BL

LMM calibration

functions and caplet volatility bootstrapping function

aaCallSnowball_LMM_fs,

aaCallSnowball_LMM_LV_fs,

aaCallSnowball_LMM_fs_tbl

Snowball valuation

functions

aaSwaption_dgen,

aaSwaption_dgen_cf,

aaSwaption2_dgen,

aaSwaption2_dgen_cf,

aaSwaption_HW,

aaSwaption_BK,

aaSwaption2_HW,

aaSwaption2_BK,

aaSwaption_MF

Short-rate

tree-based Bermudan swaption valuation functions

aaCaplet_HW,

aaCaplet_BK,

aaCaplet_MF,

aaRcap_HW,

aaRcap_BK,

aaRcap_MF,

aaSwaption_eu_HW,

aaSwaption_eu_BK,

aaSwaption_eu_MF,

aaCalibrateRcap2_HW,

aaCalibrateRcap2_BK,

aaCalibrateRcap2_MF,

aaCalibrateSwaption2_HW,

aaCalibrateSwaption2_BK,

aaCalibrateSwaption2_MF

Short rate

calibration and calibration instrument pricing functions

References

[1]

Andersen, L. and Andreasen, J. (1998),

‘Volatility Skews and Extensions of the Libor Market Model’, Mathematical Finance, 7, 127-155.

[3]

Brigo, D. and Mercurio, F. (2001), Interest Rate Models, Theory and Practice,

[4]

[5]

[6]

Jaeckel, P. (2002), Monte

Carlo Methods in Finance,

[7]

Joshi, M. (2003), The

Concepts and Practice of Mathematical Finance,

[8]

Longstaff, F. and Schwartz, E. (2001), ‘Valuing

American Options by Simulation: A Simple Least Squares Approach’, The Review of Financial Studies, 14,

113-147.

[10] Muck,

M. (2003) ‘On the Similarity between Displaced Diffusion and Constant

Elasticity of Variance Market Models of the Term Structure’, German Finance

Association 11th Annual Meeting,

[14]

Rebonato, R. (2002) Modern

Pricing of Interest-Rate Derivatives, Princeton:

Disclaimer

With respect to this document,

FinancialCAD Corporation (“FINCAD”) makes no warranty either express or

implied, including, but not limited to, any implied warranty of merchantability

or fitness for a particular purpose. In no event shall FINCAD be liable to

anyone for special, collateral, incidental, or consequential damages in

connection with or arising out of the use of this document or the information

contained in it. This document should not be relied on as a substitute for your

own independent research or the advice of your professional financial,

accounting or other advisors.

This information is subject to change

without notice. FINCAD assumes no responsibility for any errors in this

document or their consequences and reserves the right to make changes to this

document without notice.

Copyright

Copyright © FinancialCAD Corporation 2008.

All rights reserved.